If you are a US resident or business who works or does business abroad, taxes can become even more complicated than normal.

While it is usually an exciting and profitable venture to expand into international markets, it can also come with a major tax burden. And anything unexpected when it comes to taxes is usually bad news, as it can quickly have other knock-on effects.

Form 6166: IRS Certification of US Tax Residency is one way to limit a lot of these unexpected surprises.

The US government has negotiated tax treaties with countries around the world to help US residents and companies. These treaties include reduced tax withholding rates, exemption from double taxation, and exemption from certain taxes like VAT, all of which mean you’ll receive a lot more of the money you were expecting from your international venture.

However, to claim these benefits you have to prove your US resident status, which is where Form 6166 – your US tax residency certificate – comes in.

Keep reading to learn more about Form 6166. Or if you are already facing problems with your international taxes, contact us for a free and confidential consultation and find out how we can help you.

Federal taxes are one of the most complex and stressful aspects of life; international taxes are even more so. But with expert help and advice, they don’t need to be.

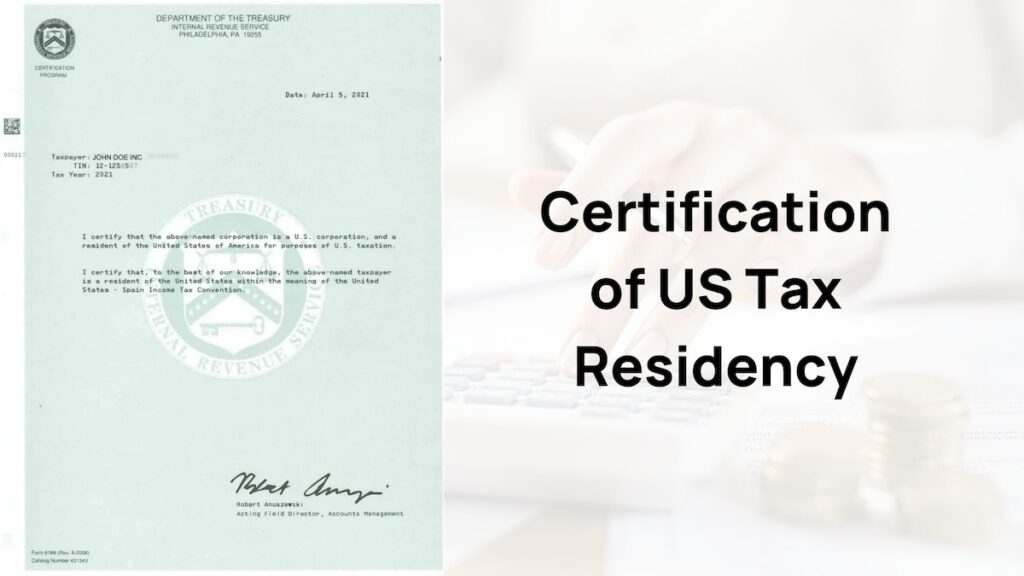

What is IRS Form 6166?

IRS Form 6166 also known as “Certification of US Tax Residency”, is an official document issued by the IRS – and printed on US Department of Treasury stationery – that certifies an individual or business entity is a resident of the United States for income tax purposes.

It’s typically needed when a US taxpayer needs to prove their residency status to a foreign tax authority to claim tax treaty benefits, such as reduced tax rates or avoiding double taxation, on any income they have earned abroad.

Somewhat confusingly, Form 6166 isn’t actually the form you need to file in order to receive this certificate. Form 6166 is the certificate. In order to request it, you need to file a separate form: Form 8802.

Why do I need a US tax residency certificate?

If you or your business does business abroad, you are entitled to a number of international tax treaty benefits that the US government has negotiated with various countries around the world.

These treaty benefits can include:

- reduced withholding tax rates (sometimes to zero)

- exemption from double taxation

- and other benefits

And apply to various forms of international income, including:

- employment wages

- interest

- retirement income

- and more

Form 6166 is also used to claim exemption from a VAT (value added tax) imposed by a foreign country.

To receive these benefits, you have to prove your eligibility to the foreign country in question, and for this, you need an official certification of US residency – a.k.a. Form 6166.

In short, a US tax residency certificate is extremely useful for any business or individual operating or working internationally, to ensure they receive the appropriate tax relief as per international agreements, and take home as much of the money they have earned as possible.

Who is eligible for Form 6166

If you are a US resident, citizen, or entity (such as a corporation, partnership, estate, or trust), you are subject to tax in the United States on your worldwide income and, as such, you are eligible for Form 6166 – as long as you also meet one of the following criteria:

- You filed an appropriate income tax return (e.g. Form 1120 for a domestic corporation) for the year in which you are requesting US residency certification.

- If you require the certification for a year in which a tax return isn’t yet due, you have filed a return for the most recent year.

- You’re not required to file an income tax return for the tax period in question, and provide other documentation as proof.

However, you are NOT eligible for Form 6166 if any of the following apply for the year in which you are requesting certification:

- You did not file a required US tax return.

- You filed a return as a non-resident.

- You are a dual-resident who has, or intends to, become a non-US-resident.

- You are a fiscally transparent entity organized in the US, without any US partners, beneficiaries, or owners.

- Your entity is an exempt organization that is not organized in the United States.

- Your entity is a trust that is part of an employee benefit plan during its first year of existence, and is not administered by a qualified custodian bank.

Essentially, anyone who needs to prove their US residency status to a foreign tax authority to claim tax treaty benefits must ensure they meet the IRS’s criteria for residency and have filed their US tax returns for the relevant period.

What is Form 8802 and how is it related to Form 6166?

As already mentioned, Form 6166 is not the form you need to complete and file with the IRS in order to receive your residency certification; it’s the letter of certification itself, which you need to submit to a foreign tax authority.

To receive Form 6166, you need to complete and submit IRS Form 8802.

Form 8802 requires details about your identity, tax identification number, and the specific tax period for which the certification is needed. It must be submitted at least 45 days before you need the certificate, and you have to pay a fee of $85 for individual applicants, and $185 for non-individual applicants.

What is Form 6166 processing time?

It typically takes around 45 days to process Form 6166, but during peak periods it can take longer, so it’s important to submit your application with plenty of time to spare.

If there will be a delay in your Form 6166 processing time, the IRS will contact you after 30 days to advise you.

It’s also important to note that your certification of US tax residency will only be valid for the year for which it is issued. If you need certification for multiple years, you must specify each year on Form 8802 when making the application.

Equally, if you require Form 6166 residency certification again in subsequent years, you need to reapply each year, with a new Form 8802.

Due to the eligibility criteria, the IRS cannot accept early submissions and will only accept applications that have a postmark date of December 1st or later of the year before the certification year required. E.g. If you are requesting Form 6166 for the year 2025, it cannot have a postmark date prior to December 1st 2024.

Get Help from Tax Experts

Navigating the intricacies of IRS forms and tax laws is complex and time-consuming, and it’s for that very reason that so many people find themselves facing unexpected tax liabilities or other problems with the IRS.

If you are facing problems with the IRS that you don’t know how to resolve, don’t suffer in silence, and definitely don’t ignore it. Seek help from tax experts.

At Tax Relief Helpers we have a team of over 100 expert tax professionals who know the ins and outs of the federal tax system, and will be able to help you resolve your tax problems in the best way possible.

Contact us today to find out more about how we can help you.